In the world of trading, the development of sophisticated algorithms has changed the landscape, enabling traders to execute complex strategies with high precision and speed. One of the critical components that underpin the success of these algorithms is backtesting. In this blog, we will delve into the importance of backtesting in algo trading software, its benefits, challenges, and best practices for conducting thorough backtests.

Understanding Backtesting

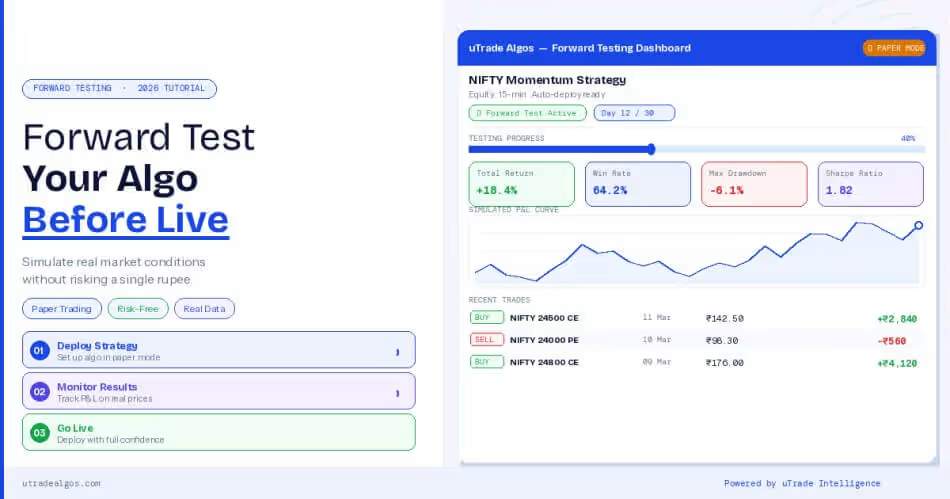

Backtesting is a simulation process where a trading strategy is applied to historical market data to assess how it would have performed in the past. The primary objective is to determine whether a trading strategy is viable and to identify any potential issues or weaknesses. By analysing historical data, traders can gain insights into how their algorithmic trading software might behave in different market conditions.

The Benefits of Backtesting

Risk Management

- One of the foremost benefits of backtesting is risk management. By simulating trades on historical data, traders can identify potential risks and evaluate the robustness of their strategies. This process helps in understanding the worst-case scenarios and prepares traders to handle unexpected market movements.

Validation of Strategies

- Backtesting allows traders to validate their strategies before committing real capital. It helps in confirming whether the strategy's logic is sound and if it performs as expected. This validation is crucial in building confidence in the algorithm's capability to execute trades effectively.

Performance Metrics

- Backtesting provides valuable performance metrics, such as win-loss ratios, drawdowns, and Sharpe ratios. These metrics offer insights into the strategy's historical performance and help traders make informed decisions about whether to proceed with the strategy in live trading.

Optimisation

- Through backtesting, traders can fine-tune their strategies to optimise performance. By adjusting parameters and testing different scenarios, traders can enhance their strategies to better adapt to varying market conditions.

Challenges in Backtesting

While backtesting is a powerful tool, it comes with its own set of challenges:

- Data Quality: The accuracy of backtesting results heavily depends on the quality of historical data. Incomplete or incorrect data can lead to misleading conclusions. It is essential to use reliable data sources and ensure data integrity.

- Overfitting: Overfitting occurs when a strategy is too closely tailored to historical data, capturing noise rather than underlying patterns. This can result in poor performance when the strategy is applied to live data. Traders must be cautious of overfitting and ensure their strategies are robust and generalisable.

- Market Changes: Historical data reflects past market conditions, which may not always be indicative of future trends. Market dynamics can change, and a strategy that performed well in the past may not necessarily do so in the future. Traders should be aware of this limitation and continuously monitor and adjust their strategies.

Best Practices for Backtesting

To maximise the effectiveness of backtesting, traders should adhere to several best practices:

- Use High-Quality Data: Ensure that the historical data used for backtesting is accurate, complete, and from reliable sources. High-quality data is crucial for obtaining meaningful and trustworthy results.

- Diversify Data Sets: Test the strategy on multiple data sets, including different time frames and market conditions. This helps in assessing the strategy's robustness and identifying any potential weaknesses.

- Incorporate Transaction Costs: Include transaction costs, such as commissions and slippage, in the backtesting process. Ignoring these costs can lead to an overestimation of the strategy's performance.

- Avoid Overfitting: Strive for simplicity in strategy design to avoid overfitting. A strategy that performs well across various market conditions is more likely to succeed in live trading.

- Regular Review and Adjustment: Backtesting should be an ongoing process. Regularly review and adjust strategies based on new data and changing market conditions to ensure continued effectiveness.

Backtesting on Algo Trading Platforms

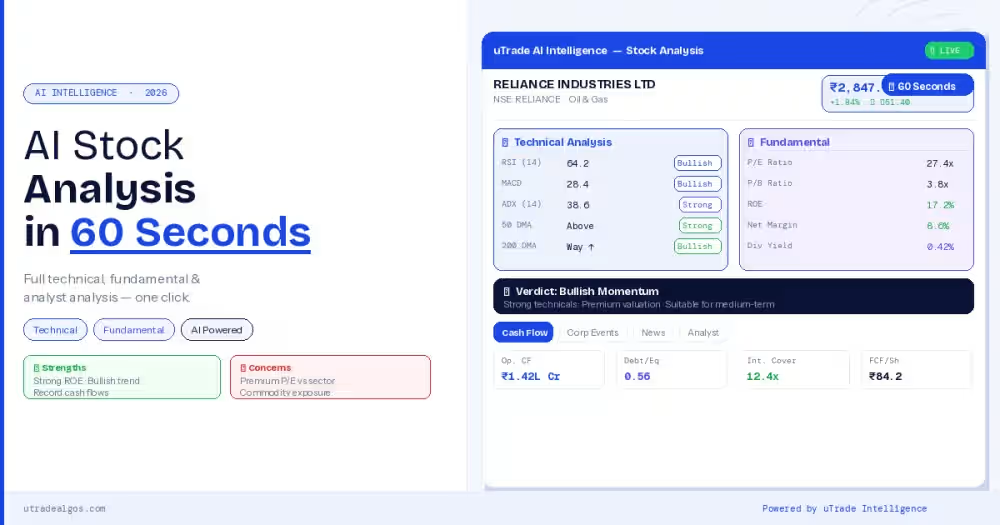

The best algorithmic trading software are those that offer advanced backtesting capabilities that empower traders to rigorously test and optimise their strategies. These platforms provide access to extensive historical data, sophisticated analytical tools, and customisable testing environments.

- Comprehensive Data Access: uTrade Algos offers access to a wide range of historical market data, enabling traders to test their strategies on diverse data sets. This comprehensive data access is essential for evaluating strategy performance across different market conditions.

- Advanced Analytical Tools: Such platforms provide a suite of analytical tools that facilitate in-depth analysis of backtesting results. Traders can use these tools to generate detailed performance reports, visualise trade outcomes, and identify areas for improvement.

- Customisable Testing Environments: Herein traders can customise their backtesting environments to match their specific requirements. This flexibility ensures that traders can tailor the backtesting process to align with their unique strategies and objectives.

- Integration with Live Trading: Once a strategy has been thoroughly backtested, it can be seamlessly transitioned to live trading. This integration streamlines the process of moving from simulation to real-world execution, enhancing overall trading efficiency.

Future of Backtesting in Algorithmic Trading Software

As technology continues to evolve, the future of backtesting in algorithmic trading software looks promising. Advances in artificial intelligence (AI) and machine learning (ML) are expected to further enhance the capabilities of backtesting tools. AI and ML can analyse vast amounts of data, identify complex patterns, and provide more accurate predictions, leading to more effective backtesting and strategy optimisation.Moreover, the integration of backtesting with blockchain technology and decentralised finance (DeFi) platforms could revolutionise the trading industry. Blockchain's transparency and security features can enhance the trustworthiness of backtesting results, while DeFi platforms offer new opportunities for algorithmic trading in decentralised markets.

Backtesting is an indispensable component of algo trading software, playing a crucial role in validating, optimising, and managing trading strategies. By simulating trades on historical data, traders can gain valuable insights into their strategies' performance and make informed decisions about their viability in live trading. Platforms like uTrade Algos provide the tools and resources necessary to conduct rigorous backtesting, empowering traders to achieve their trading goals with greater confidence.