In the fast-paced world of financial markets, traders and investors are constantly seeking an edge to stay ahead of the curve. Algorithmic trading, or algo trading, has emerged as a powerful tool to gain this competitive advantage. It involves the use of automated trading systems, often fuelled by complex algorithms, to execute trades with speed and precision. However, before deploying these algorithms in live markets, algo traders employ a crucial step to evaluate and fine-tune their strategies: backtesting. Here, we will find out what algo backtesting is and how it works.

Defining Algo Backtesting

Algo backtesting is a systematic process that allows traders to assess the performance of their trading strategies using historical data. By simulating past market conditions and applying their trading rules to historical price and volume data, traders can gain valuable insights into how their strategies would have fared in the real world. It involves the following fundamental steps:

Strategy Development

Traders and developers meticulously craft a set of rules and conditions that constitute the trading strategy. These rules encompass a variety of aspects:

- The specific conditions that determine when a trade is initiated (buy) and when it is exited (sell).

- Guidelines for managing risk, including stop-loss orders, take-profit levels, and position sizing to control potential losses.

- Determining how much capital is allocated to each trade and how it varies based on risk and market conditions.

- The strategy may incorporate technical indicators, which are used to gain insights into market trends, momentum, and potential reversal (e.g., moving averages, Relative Strength Index) and chart patterns (visual representations of historical price movements and are used to predict future price direction) to generate trade signals.

Historical Data Acquisition

Traders need to obtain reliable historical data for the financial assets they intend to trade, such as stocks, commodities, or forex pairs. Ensuring the historical data is clean and accurate is important, as poor data quality can distort backtesting results. This is where platforms like uTrade Algos become important as they provide reliable historical data.

Strategy Simulation

- Traders apply the pre-defined strategy rules to the historical data in a systematic manner. They execute trades according to the strategy's criteria and track each trade's entry and exit points, position sizes, and trading costs.

- The simulation occurs in a historical context, with the strategy reacting to past market conditions. This process continues throughout the entire historical dataset, simulating how the strategy would have performed over that time period.

Performance Evaluation

After the simulation, traders perform a comprehensive analysis of the strategy's historical performance. Key performance metrics are calculated, including:

- Total Return on Investment (ROI): The total profit or loss generated by the strategy over the historical period.

- Maximum Drawdown: The largest peak-to-trough loss experienced by the strategy.

- Risk-Adjusted Returns: Measures like the Sharpe ratio are considered, which assess the strategy's return in relation to the level of risk taken.

- Trade-Level Analysis: Traders examine individual trades to understand their contribution to the overall performance, helping to identify patterns of success and failure.

Strategy Refinement

- Based on the performance analysis, traders may choose to refine the strategy. This process involves making adjustments to different elements of the strategy.

- Traders may fine-tune strategy parameters, such as stop-loss levels, take-profit levels, or timeframes used by technical indicators, to enhance performance.

- Changes to the entry and exit criteria or risk management rules can be made to adapt the strategy to evolving market conditions.

- In some cases, traders may overhaul the entire strategy if it consistently underperforms, leading to a new strategy development cycle.

How Does Algo Backtesting Work?

Data Preparation

- The first step in algo backtesting is meticulous data collection and preparation.

- Historical data for the assets or instruments intended for trading must be gathered.

- This data typically includes not only price and volume information but should also be meticulously cleaned and adjusted for corporate actions, such as stock splits and dividends.

- The accuracy of the data is paramount since the quality of the backtest is heavily reliant on the quality of the input data.

Strategy Coding

- The heart of algo strategy backtesting lies in coding the trading strategy.

- Traders or developers write the trading rules into a computer program.

- This program should include a comprehensive set of instructions, including entry and exit rules, risk management parameters, position sizing rules, and any other relevant conditions.

- Various programming languages can be used for this purpose, with Python and R being popular choices due to their versatility and data analysis capabilities.

- Nowadays, there are various strategy backtesting platforms, like uTrade Algos, and tools available that allow traders and investors to conduct backtesting without having to write code. These platforms often provide a range of technical indicators and parameters that can be customised without writing code. Here, you can configure various parameters of your selected strategy. For example, you can specify entry and exit conditions, risk management settings, and position sizing rules. Most platforms allow you to do this through simple drop-down menus or settings.

Simulation

- The coded trading strategy is then applied to the prepared historical data within a simulated environment.

- The program processes each data point sequentially, making trading decisions based on the rules defined in the code.

- When a buy or sell signal is generated, the program records the trade, along with critical data such as entry and exit prices, dates, and positions.

- This process continues until the entire historical dataset is simulated.

Performance Metrics

- After the simulation is completed, the program calculates a range of performance metrics.

- These metrics serve as the yardstick for evaluating the strategy's historical performance. Metrics often include total return on investment (ROI), maximum drawdown (the peak-to-trough decline in capital), the Sharpe ratio (which measures risk-adjusted returns), and others.

- These metrics provide invaluable insights into how the strategy would have performed in the past.

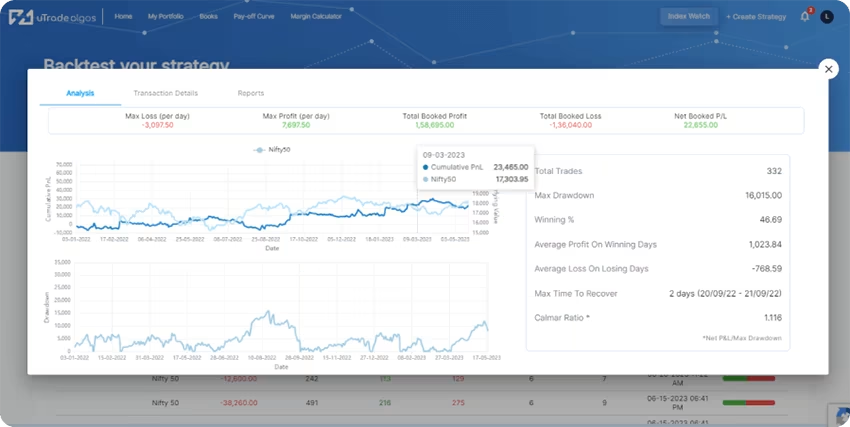

Visualisations

- Backtesting platforms typically provide visual representations of the strategy's equity curve.

- For example, on the uTrade Algos strategy backtesting platform, you can use interactive payoff curves to find out how changes in parameters will affect the potential outcomes of your trades.

- The visual display showcases how the trading capital would have grown or declined over time.

- Additionally, traders can delve into detailed trade-by-trade performance analysis, which enables them to identify the strengths and weaknesses of the strategy.

Optimisation

- Based on the results of the initial backtest, traders may opt for strategy optimisation.

- This involves tweaking parameters or refining rules to enhance the strategy's performance.

- However, caution is essential during optimisation to prevent overfitting, which can make the strategy perform well in historical data but poorly in real markets.

Out-of-Sample Testing

- To validate the robustness of the strategy, traders often perform out-of-sample testing.

- This step entails applying the strategy to a separate set of historical data that was not used during the initial backtest.

- The goal is to assess whether the strategy can generalise beyond the specific historical dataset used for the primary backtest.

Walk-Forward Testing

- For traders who seek adaptability and resilience in their strategies, walk-forward testing is employed.

- This approach involves periodic re-optimisation of the strategy and testing it on a new, forward-looking dataset.

- This dynamic process aims to ensure that the strategy can adapt to evolving market conditions and continue to perform well in changing environments.

Algorithmic backtesting represents a vital phase in the world of algorithmic trading, where precision and data-driven decisions are paramount. This meticulous and systematic process indeed empowers traders and developers to scrutinise the potential of their trading strategies, offering a window into how these strategies would have performed in historical market conditions. It is that crucial bridge between theory and practice that allows traders to have confidence in their strategies before committing to real capital. So don’t forget to backtest your algo strategies!